Open Finance: The Evolution from Sharing Bank Data to Sharing Insurance, Mortgages, and Pensions

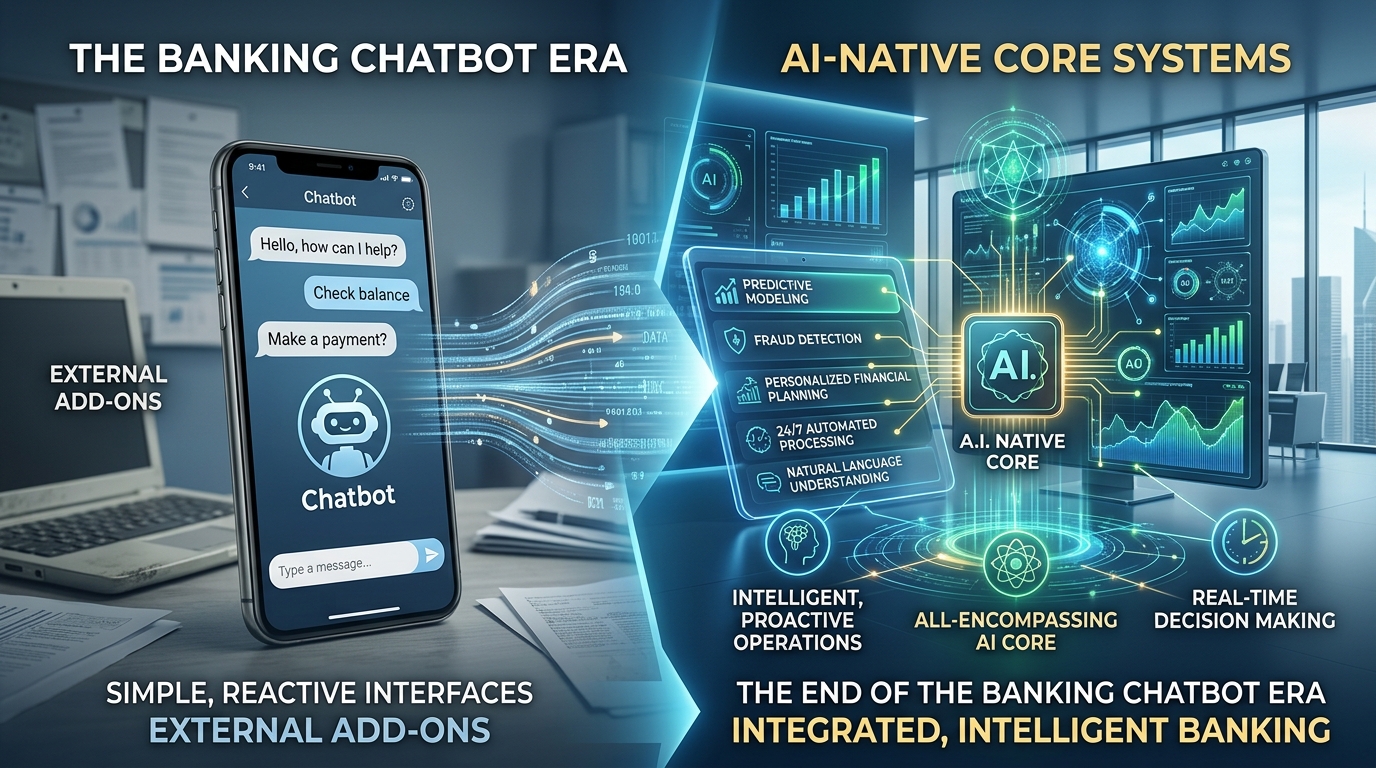

For the past several years, Open Banking has been a quiet revolution. It allowed consumers to share their transaction history securely with third-party apps—think budgeting tools, loan pre-approvals, and account aggregators. That was phase one.

Now, a far more powerful shift is underway: Open Finance.

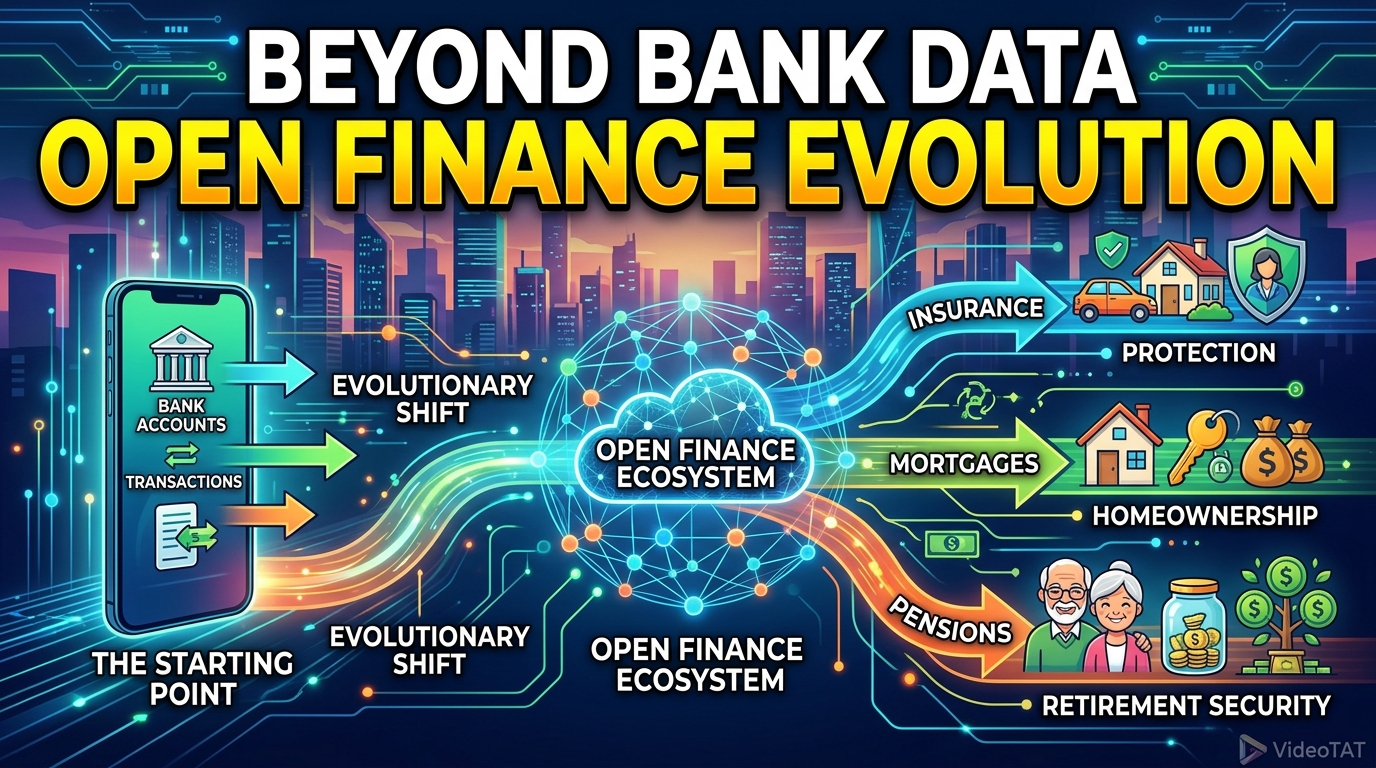

Open Finance expands the scope of data sharing far beyond bank accounts. It includes insurance policies, mortgage balances, pension portfolios, investment accounts, utility bills, and even crypto exchange holdings. The goal is simple yet transformative: give consumers and businesses the ability to securely share their complete financial lives with approved providers, unlocking personalized products, lower costs, and real-time decision-making.

For the current generation—digital natives who expect personalization, portability, and control—Open Finance is not an abstract regulatory concept. It is the key to finally owning their financial identity.

Below, we explore how Open Finance evolves from Open Banking, what new data types are included, real-world applications for today’s audience, and why this shift matters for everyone from gig workers to mortgage seekers.

Part 1: From Open Banking to Open Finance – A Natural Evolution

To understand Open Finance, you must first understand what came before.

1.1 What Was Open Banking?

Open Banking emerged from regulations (such as PSD2 in Europe and similar frameworks elsewhere) that required banks to expose customer data via secure APIs (Application Programming Interfaces). With a customer’s consent, a third-party app could read transaction data, check balances, and even initiate payments.

- What it enabled: Budgeting apps (e.g., Mint, YNAB), automated accounting for small businesses, and instant loan underwriting based on cash flow.

- Limitations: Only bank account data (checking, savings, credit card transactions). No visibility into wealth, protection, or long-term liabilities.

1.2 What Is Open Finance?

Open Finance takes the same legal and technical framework—consumer consent, API-based sharing, strict security standards—and applies it to the rest of the financial system.

- Keyword highlight: Open Finance is the expansion of data-sharing rights to include insurance, mortgages, pensions, investments, and other regulated financial products.

- Current status: Pilots and live implementations exist in the UK, Brazil, Australia, and parts of the European Union. Consumer demand is pushing regulators and financial institutions to move faster.

Why the current generation cares: A young professional may have a bank account, a 401(k) or pension, a renters insurance policy, and a student loan. Open Finance lets them see and use all of these together, not as silos.

Part 2: New Data Pillars in Open Finance

While Open Banking focused on transaction accounts, Open Finance introduces four major new categories of consumer-permissioned data.

2.1 Insurance Data

Your insurance policies are financial products, yet they have historically lived apart from your banking data. Open Finance changes that.

- What is shared: Policy terms, coverage limits, premium amounts, claims history, renewal dates, and beneficiary information for auto, home, renters, life, and health insurance.

- How it helps:

- An Open Finance-enabled comparison tool can analyze your existing coverage and instantly recommend better or cheaper policies without manual data entry.

- Insurers can offer usage-based insurance (e.g., pay-per-mile auto) by securely accessing driving patterns from a connected app, with your consent.

- Claims processing becomes faster: an insurer can verify bank account details and policy history in seconds.

- Keyword highlight: Embedded insurance and Open Finance together enable real-time policy optimization—adjusting coverage as your life changes (new car, new apartment, new child).

2.2 Mortgage Data

Your mortgage is likely your largest liability. In Open Finance, it becomes a shareable data point.

- What is shared: Outstanding balance, interest rate, payment history, maturity date, property value estimates, and equity accrued.

- How it helps:

- Refinancing: A lender can pull your current mortgage terms with one click and offer a lower rate without requiring uploaded PDF statements.

- Debt consolidation: An app can see your mortgage, credit card, and auto loan balances together and simulate consolidation scenarios.

- Home equity products: You can instantly qualify for a home equity line of credit (HELOC) by sharing real-time mortgage and income data.

- Keyword highlight: Mortgage data sharing via Open Finance reduces refinancing friction from weeks to minutes.

2.3 Pension and Retirement Data

For the current generation, retirement feels distant but urgent. Open Finance makes pension and retirement data visible and actionable.

- What is shared: Contribution history, current balance, investment allocation, projected retirement income, employer match details, and vesting schedule.

- How it helps:

- A financial wellness app can aggregate an employer-sponsored 401(k), an IRA, and a state pension into a single dashboard.

- Job changers can see the impact of leaving a pension plan before making a decision.

- Automated advisors (robo-advisors) can recommend contribution increases based on real-time spending and savings data from your bank account.

- Keyword highlight: Pension aggregation through Open Finance gives workers a complete picture of their future, not just their checking account.

2.4 Investment and Crypto Data

Modern portfolios include stocks, bonds, ETFs, and increasingly crypto assets. Open Finance includes them all.

- What is shared: Holdings, transaction history, realized/unrealized gains, dividend payments, and exchange wallet balances (including crypto).

- How it helps:

- Tax preparation: An app can pull investment transactions and crypto trades to estimate capital gains.

- Portfolio rebalancing: A robo-advisor can see your holdings across multiple brokers and recommend adjustments.

- Collateralized lending: You can prove crypto or stock ownership to secure a loan without selling assets.

- Keyword highlight: Multi-asset aggregation is a core promise of Open Finance, bridging traditional finance and digital assets.

Part 3: How Open Finance Benefits the Current Generation

The shift from Open Banking to Open Finance is not a technical footnote. It directly addresses the frustrations and aspirations of today’s consumers.

3.1 True Financial Portability

Younger users change jobs, cities, and financial providers frequently. Open Finance makes it possible to leave a bank, insurer, or pension provider without losing your data history.

- Example: You switch auto insurers. With Open Finance, your new insurer requests your claims history directly from your old insurer (with your permission). No phone calls, no waiting on hold.

3.2 Personalized Financial Products at Scale

Algorithms thrive on data. More data (insurance, mortgage, pension, investments) means better personalization.

- Real-world use case: A freelancer with irregular income wants a mortgage. An Open Finance-enabled lender analyzes two years of bank transactions, plus renters insurance history (showing reliability) and pension contributions (showing long-term stability). The lender offers a tailored mortgage that traditional underwriting would have denied.

3.3 End of Manual Data Entry

The current generation hates forms. Open Finance eliminates repetitive data entry.

- Applying for a loan: Instead of uploading bank statements, insurance declarations, and investment account screenshots, you click “Share via Open Finance.”

- Buying a home: Your mortgage broker accesses your bank, insurance, and pension data in one consent flow.

3.4 Better Financial Health Dashboards

Apps like Copilot, Monarch, and Lunch Money already aggregate bank accounts. Open Finance adds the missing pieces:

- Your insurance deductibles and coverage gaps.

- Your mortgage payoff progress and refinancing opportunities.

- Your pension projected income alongside your current savings rate.

Keyword highlight: Holistic financial dashboards powered by Open Finance replace fragmented spreadsheets and multiple logins.

Part 4: Real-World Applications and Events (Current)

Open Finance is not a future promise. It is happening now, with live implementations and clear momentum.

4.1 Brazil’s Open Finance Journey

Brazil already leapfrogged many nations with Pix (real-time payments). Now, Brazil is implementing one of the world’s most ambitious Open Finance frameworks.

- Scope: Includes bank accounts, credit cards, investments, insurance, pensions, and foreign exchange.

- Current status: Multiple phases live, with millions of consents already registered.

- Why it matters: Brazil proves that Open Finance works in a large, diverse economy with high mobile penetration.

4.2 United Kingdom – The Next Frontier

The UK pioneered Open Banking. Now regulators are consulting on a full Open Finance regime.

- Proposed data sets: Insurance, mortgages, savings, investments, and pensions.

- Consumer benefit: A single “financial passport” that allows any regulated provider to serve you better.

- Timeline: Implementation rolling out, with major fintechs already building Open Finance-ready products.

4.3 Australia’s Consumer Data Right (CDR)

Australia extended its Consumer Data Right from banking to energy and is now moving into insurance and pensions.

- Unique feature: Consumers can not only share data but also direct that data to be transferred to a new provider (switching).

- Keyword highlight: Consumer Data Right is Australia’s brand of Open Finance, and it includes pension data sharing as a priority.

Part 5: Security, Consent, and Privacy in Open Finance

With more data comes more responsibility. Open Finance is built on a foundation of granular consent and strong authentication.

5.1 How Consent Works

Unlike screen scraping (which often required sharing login credentials), Open Finance uses OAuth-like tokens.

- You control: What data is shared, with whom, and for how long (e.g., 90 days).

- Revocable: You can withdraw consent at any time through a dashboard or app.

- Auditable: Every data access request is logged.

5.2 Who Can Participate

Not just anyone can request Open Finance data. Providers must be:

- Regulated (e.g., by a financial conduct authority).

- Certified for security (e.g., ISO 27001, SOC 2).

- Transparent about how data will be used.

Keyword highlight: Regulated access ensures that Open Finance does not become a privacy nightmare. Bad actors are excluded.

5.3 Current Generation Expectations

Younger users are willing to share data—but only for clear value and with full transparency. Open Finance meets this demand by replacing “consent buried in fine print” with click-by-click permission.

Part 6: Challenges and the Road Ahead

No transformation is seamless. Open Finance faces several hurdles.

6.1 Inconsistent Global Standards

While Brazil, the UK, and Australia advance, many countries still lack Open Banking, let alone Open Finance. Cross-border Open Finance remains rare.

- Solution: International standards bodies (e.g., FDX, Open Future World) are working on common APIs.

6.2 Legacy Technology at Insurers and Pension Funds

Banks have modernized APIs. Many insurance companies and pension administrators run on decades-old mainframes. Exposing data via APIs is expensive and slow.

- Current trend: Regulatory deadlines and fintech partnerships are forcing modernization.

6.3 Consumer Awareness

Ask a typical smartphone user what Open Finance means, and they will likely shrug. Adoption depends on clear, tangible benefits—not jargon.

- What works: Marketing “one-click refinancing” or “see all your pensions in one place” instead of leading with the term Open Finance.

Conclusion: Your Financial Life, Unlocked

Open Banking gave us a window into our transaction accounts. Open Finance opens the entire house: insurance policies that protect us, mortgages that house us, pensions that retire us, and investments that grow our wealth.

For the current generation, this evolution means freedom from silos, freedom from paperwork, and freedom to choose the best provider for every financial need—without switching costs.

The future of finance is not about more products. It is about better access to the data that connects them. That future is called Open Finance, and it is arriving faster than most people realize.

Keywords: Open Finance, Open Banking, insurance data sharing, mortgage data sharing, pension data aggregation, investment data access, crypto asset aggregation, holistic financial dashboards, real-time policy optimization, Consumer Data Right, regulated access, multi-asset aggregation, pension integration, embedded insurance.

Unlock Financial Freedom: Why Every Entrepreneur Needs Business Credit