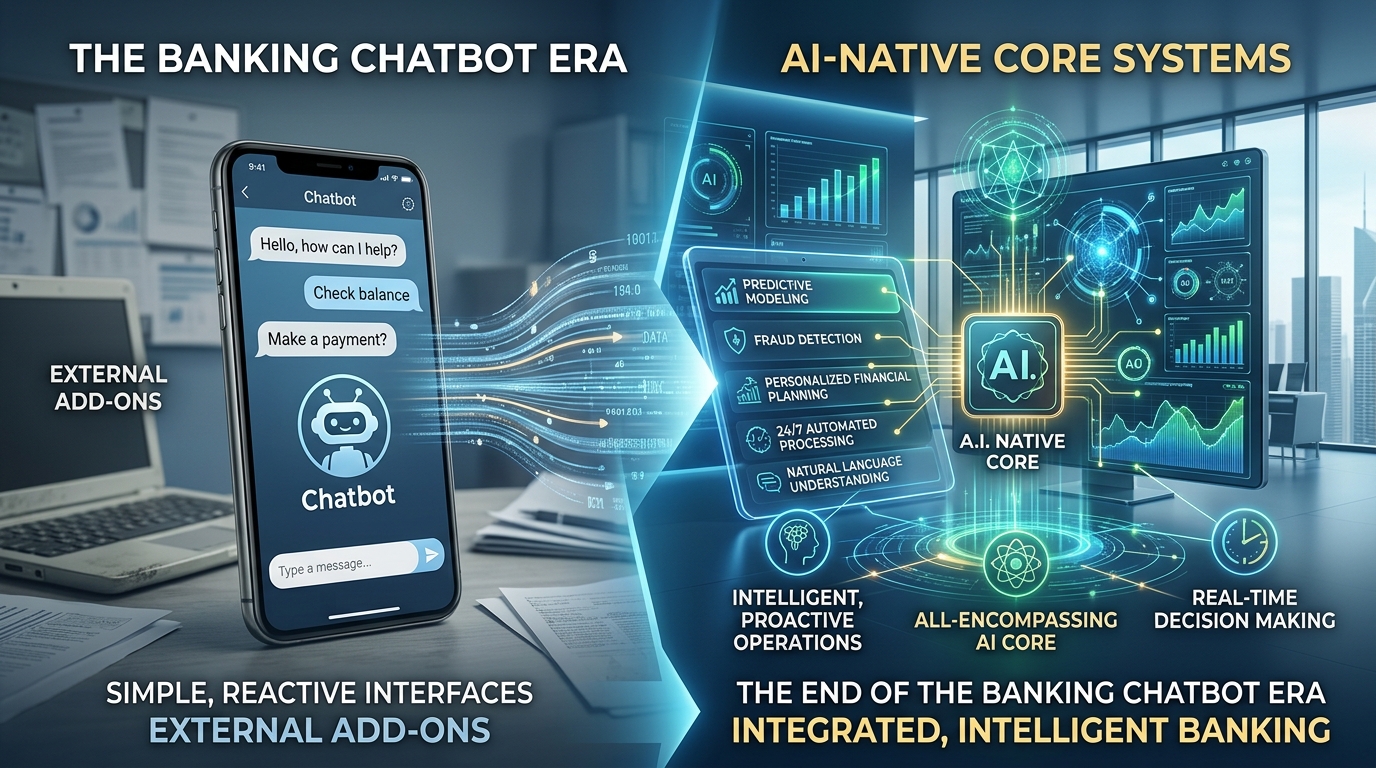

AI-Native Core Systems: The End of the Banking Chatbot Era

The financial industry is standing at a critical crossroads. For years, the conversation around artificial intelligence in banking has been dominated by a single, surface-level image: the friendly chatbot. Whether answering account balance inquiries or resetting passwords, these conversational agents have become the public face of “AI in finance.” But beneath this shallow interface, a far more profound transformation is already underway.

Welcome to the era of the AI-native core system—a fundamental re-architecture of banking infrastructure where artificial intelligence is not an add-on or a front-end gimmick, but the central processing engine itself.

From Front-End Gimmicks to Core Intelligence

The Limitations of Legacy Chatbots

Traditional chatbots are, at best, a thin layer of automation. They operate on predefined rules, keyword triggers, or lightweight natural language models. When a customer asks, “What’s my current balance?” the chatbot queries a legacy core database and returns a static answer. When the request becomes complex—“Should I move $5,000 from savings to checking to avoid overdraft before my mortgage auto-pays tomorrow?”—most chatbots fail. They cannot reason, predict, or act in real time.

These tools were never designed to touch the transaction workflow or risk management engines of a bank. They sit in a silo, offering conversation without consequence. The current generation of digital-native customers has already grown impatient with this limitation. They want instant, intelligent, and proactive financial management—not a polite robot that reads numbers aloud.

Defining the AI-Native Core System

An AI-native core system is radically different. Here, AI is not connected via APIs to a legacy mainframe. Instead, the core banking ledger, transaction processing engine, and risk assessment modules are built from the ground up around machine learning models. These models continuously learn from every transaction, every authorization, every failed payment, and every customer interaction.

In this architecture, real-time transaction workflows are managed dynamically by AI agents. There is no batch processing. No overnight settlement delays. No manual rule-setting for fraud alerts. The system observes, predicts, and acts—within milliseconds.

How AI Manages Real-Time Transaction Workflows

Dynamic Routing and Optimization

Imagine a customer using their debit card at a coffee shop. Under a legacy system, the transaction travels a fixed path: authorization request → balance check → fraud rule evaluation → approval or decline. The entire process is binary and rigid.

In an AI-native core, the same transaction triggers a parallel set of intelligent actions:

- The AI checks not just the balance but also predicted cash flow for the next 48 hours.

- It evaluates the merchant’s historical risk profile and the customer’s current location against behavioral patterns.

- It decides in real time whether to approve, flag, or even reroute the transaction through a different funding source (e.g., a linked credit line) to avoid an overdraft fee.

This is intelligent transaction orchestration—a shift from passive processing to active, AI-led workflow management.

Predictive Adjustments Before the Customer Acts

Perhaps the most powerful feature of an AI-native core is anticipatory execution. Instead of waiting for a transaction to occur, the system continuously models likely scenarios. For example:

- A subscription payment is due in six hours, but the checking account balance is low.

- The AI predicts a high probability of declined payment based on historical spending patterns.

- It then automatically moves funds from a savings or credit buffer, notifies the user, and processes the payment seamlessly.

No chatbot is involved. No manual transfer is required. The core system itself has become the intelligent agent.

Risk Management Reimagined: AI as the First Line of Defense

Real-Time Risk Scoring That Evolves

Traditional banking risk systems rely on static rules and periodic model updates—sometimes refreshed only once a quarter. By then, new fraud patterns have already emerged. AI-native cores invert this model.

Every transaction becomes a data point for continuous learning. Risk scoring happens in real time, with models updating after every authorization. Behavioral biometrics, device fingerprinting, and transaction velocity are weighted dynamically. A payment that appears normal at 9 AM might be flagged by 9:05 AM if the AI detects a subtle shift in typing rhythm or location metadata.

From Fraud Detection to Fraud Prevention

Legacy systems detect fraud after it happens—or at best, during the transaction. AI-native cores aim for prevention before initiation. By analyzing sequences of micro-events (e.g., login attempt → account detail change → small test transaction), the system can intervene before the actual fraudulent transfer is attempted.

This is accomplished through autonomous risk agents—specialized AI modules running inside the core. These agents communicate with transaction workflow managers, blocking or delaying suspicious actions without human review unless absolutely necessary.

Why Current-Generation Audiences Demand AI-Native Banking

The Expectation of Invisible Intelligence

Today’s banking customers—especially digital natives who have grown up with streaming recommendations, real-time navigation, and predictive text—no longer marvel at a chatbot. They expect their bank to be invisible and intelligent. They want:

- Instant decisions, not “please wait 24–48 hours.”

- Proactive safeguards, not reactive alerts.

- Personalized cash flow management, not generic budgeting tips.

An AI-native core delivers exactly that. It removes friction by thinking ahead. For a customer who splits rent with roommates, the system might notice recurring Venmo requests and automatically reserve funds. For a freelancer with irregular income, it might adjust credit limits based on projected invoices rather than past monthly averages.

Trust and Transparency in AI-Led Banking

Of course, a fully autonomous core raises important questions about explainability and control. The current generation values transparency as much as convenience. Therefore, AI-native cores must include interpretability layers—dashboards that show why a transaction was rerouted, why a risk score increased, or why a credit line was adjusted.

Leading implementations now offer natural language explanations generated directly by the core’s AI, not a separate chatbot. The customer asks, “Why did you move $200 from my savings?” and the core responds in plain English, referencing specific patterns and predictions.

Technical Architecture: What an AI-Native Core Looks Like

Embedded Machine Learning Pipelines

Unlike legacy cores that bolt on ML models via middleware, an AI-native core integrates inference engines directly into the transaction log. Every write to the ledger is accompanied by feature updates for the models. This event-driven architecture ensures that the AI never works with stale data.

Real-Time Model Serving

Low latency is non-negotiable. AI-native cores use optimized model servers (e.g., TensorFlow Serving or custom inference runtimes) that run alongside the database. A typical transaction might involve five to ten model inferences: fraud risk, liquidity prediction, customer sentiment, merchant trust score, and more—all under 50 milliseconds.

Continuous Learning Without Downtime

These systems support online learning, where model weights are updated incrementally after each batch of transactions. There is no “retraining window” or scheduled downtime. The core evolves minute by minute, adapting to new spending habits, emerging fraud vectors, and changing economic conditions.

Moving Beyond the Chatbot: A Call to Action for Financial Leaders

The Competitive Divide Is Already Here

While some banks still invest in smarter chatbots as a differentiator, the real gap is forming at the infrastructure level. Institutions that migrate to or build AI-native cores will offer products that seem like magic to customers: instant loan decisions based on real-time cash flow, overdraft prevention that never fails, and risk management that feels prescient.

Those that do not will remain trapped in a cycle of incremental improvements—adding voice assistants to creaky mainframes, apologizing for processing delays, and losing the trust of a generation that expects more.

Practical First Steps

Transitioning to an AI-native core is not a weekend project, but financial institutions can begin today:

- Decouple transaction workflows from legacy ledgers by introducing an event-driven middleware layer that feeds real-time data to AI models.

- Run parallel AI risk agents alongside existing fraud systems to validate performance before full migration.

- Replace static customer rules (e.g., “alert me if balance < $100”) with adaptive policies managed by AI.

- Retrain teams to think in terms of AI-orchestrated processes, not chatbot scripts.

Conclusion: The Core Is the Chat Now

The most successful banking AI of the coming years will not talk to you. It will work for you silently, instantly, and intelligently—inside the core system itself. The chatbot was a stepping stone, not a destination. The future belongs to AI-native cores where real-time transaction workflows and risk management are inseparable from the ledger.

For today’s customers, the best conversation is no conversation at all. Just a bank that finally understands them before they even ask.

https://www.youtube.com/@videotat-documentary