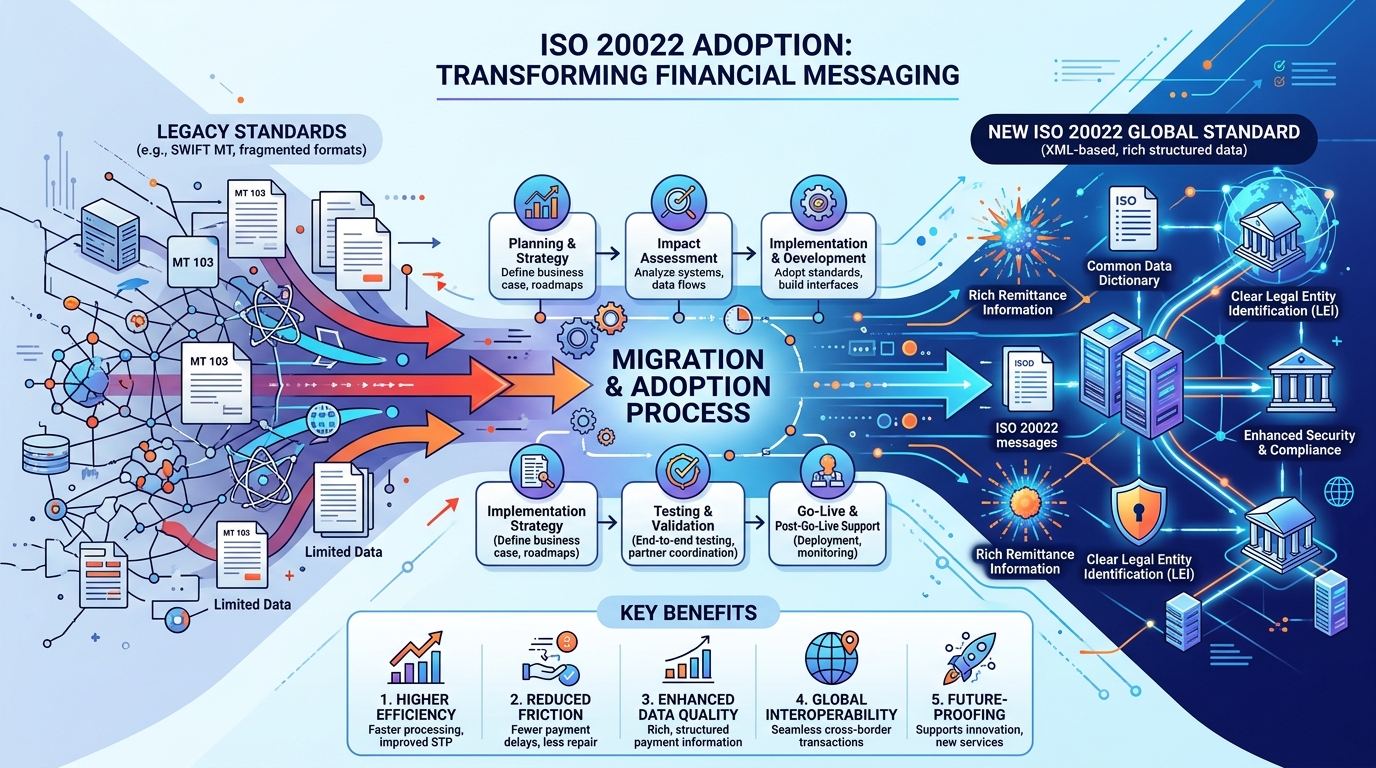

ISO 20022 Adoption: The Global Transition to a New Standard for Electronic Data Interchange

For decades, the world’s financial institutions have communicated using a patchwork of outdated, inconsistent, and limited messaging formats. SWIFT MT messages—those rigid, character-limited, often cryptic transmissions—have been the backbone of cross-border and high-value payments. That era is ending.

A fundamental shift is underway: ISO 20022 adoption is transforming how banks, payment systems, and financial infrastructures exchange data. This new global standard for electronic data interchange replaces fragmented legacy protocols with a rich, structured, and extensible language. It is not a minor upgrade. It is a complete reimagining of financial messaging.

ISO 20022 enables far more data to travel with every payment: remittance information, invoice details, regulatory reporting fields, and even environmental, social, and governance (ESG) markers. For the current generation of finance professionals, developers, and business leaders, understanding ISO 20022 is no longer optional. It is essential for compliance, operational efficiency, and building next-generation financial products.

Below, we explore what ISO 20022 is, why the transition is happening now, how it impacts different stakeholders, and what the current generation needs to do to prepare.

Part 1: What Is ISO 20022?

Before diving into the adoption timeline and technical details, it is essential to understand the standard itself.

1.1 Defining the Standard

ISO 20022 is an international standard for electronic data interchange between financial institutions. Unlike previous standards that used fixed field lengths and limited code sets, ISO 20022 uses a XML-based (Extensible Markup Language) and later JSON (JavaScript Object Notation) syntax. This allows for:

- Rich data: Up to 900 characters of remittance information compared to legacy limits of 140 characters.

- Structured fields: Instead of a single “notes” field, data is organized into clear categories (e.g., invoice number, purchase order date, tax amount).

- Global interoperability: The same message format works for payments, securities, trade finance, and card transactions.

- Keyword highlight: ISO 20022 is a common financial language that replaces dozens of incompatible dialects.

1.2 How It Differs from Legacy Standards (SWIFT MT)

Most financial professionals are familiar with SWIFT MT messages (e.g., MT103 for customer transfers, MT202 for bank-to-bank transfers). These were designed decades ago with severe constraints.

| Feature | Legacy SWIFT MT | ISO 20022 (MX) |

|---|---|---|

| Character limit per field | 35–140 characters | Up to 9,000+ characters |

| Data structure | Flat, positional | Hierarchical (XML/JSON) |

| Remittance details | Concatenated into one field | Separate fields for invoice, tax, shipping |

| Machine readability | Low (requires manual parsing) | High (native API/XML parsing) |

| Upgrade path | Fixed by SWIFT | Open standard, extensible |

Why the current generation cares: Legacy standards force developers to write fragile parsers. ISO 20022 produces clean, machine-readable data that integrates directly into modern accounting, fraud detection, and reconciliation systems.

Part 2: The Global Shift – Who Is Adopting ISO 20022?

ISO 20022 adoption is not a single event. It is a coordinated, worldwide transition across multiple payment systems and networks.

2.1 SWIFT’s High-Value Payments Transition

SWIFT, the cooperative that powers most cross-border and high-value payments, has mandated the transition to ISO 20022 for all MT messages on its network.

- What changed: Correspondent banks, treasury departments, and large corporates must now send and receive ISO 20022 (MX) messages for cross-border payments. The legacy MT standard is being phased out.

- Current status: Many institutions are in co-existence mode, handling both MT and MX. The final transition eliminates MT entirely for most message types.

- Keyword highlight: SWIFT ISO 20022 adoption is the single largest messaging upgrade in the history of cross-border finance.

2.2 Major Real-Time Payment Systems

Several of the world’s largest real-time payment systems have already built their infrastructure on ISO 20022 or are actively migrating.

- FedNow (US): The Federal Reserve’s instant payment system uses ISO 20022 as its native message format.

- Pix (Brazil): Brazil’s wildly successful instant payment network is based on ISO 20022.

- UPI (India): While UPI has its own lightweight format, India’s high-value systems (e.g., RTGS) are migrating to ISO 20022.

- TARGET Services (Eurozone): The European Central Bank’s real-time gross settlement system (TARGET2) and TARGET Instant Payment Settlement (TIPS) are fully ISO 20022-compliant.

- Keyword highlight: Real-time payments and ISO 20022 are converging, enabling instant, data-rich transactions globally.

2.3 Domestic and Regional Clearing Systems

Beyond the headline systems, dozens of domestic Automated Clearing Houses (ACHs), securities settlement systems, and card networks are transitioning.

- Examples: The US’s CHIPS, the UK’s CHAPS, Australia’s NPP, and Canada’s Lynx have all announced or completed ISO 20022 adoption roadmaps.

- Keyword highlight: Electronic data interchange modernization is a global phenomenon, not limited to any single region.

Part 3: Why ISO 20022 Matters for the Current Generation

The transition to ISO 20022 is not a back-office technical change. It has profound implications for businesses, developers, and end consumers.

3.1 For Businesses: Smarter, Faster Reconciliation

One of the biggest pain points in corporate finance is payment reconciliation. A customer sends $10,000, but the remittance information is truncated or missing. Accounts receivable teams spend hours matching payments to invoices.

ISO 20022 solves this by carrying structured remittance data:

- Invoice number in a dedicated field.

- Purchase order number in another.

- Tax amount separately.

- Discounts or adjustments clearly marked.

- Benefit: Automated reconciliation becomes truly possible. Enterprise resource planning (ERP) systems can ingest ISO 20022 messages directly, eliminating manual keying.

- Keyword highlight: Structured remittance dramatically reduces days sales outstanding (DSO) and cuts operational costs.

3.2 For Developers and Fintechs: Clean APIs and Less Parsing

Legacy financial messaging is a nightmare for modern software development. Fixed-width fields, ambiguous code values, and inconsistent date formats require endless custom parsing logic.

ISO 20022 messages are XML or JSON. They can be consumed by any modern programming language (Python, Java, Go, Rust) with standard libraries.

- What developers gain:

- No more “magic numbers” or position-based slicing.

- Built-in validation via XML schemas or JSON schemas.

- Native support for webhooks, REST APIs, and event-driven architectures.

- Keyword highlight: Developer-friendly standards accelerate fintech innovation. ISO 20022 is the first global financial standard designed for the API era.

3.3 For Compliance and Anti-Financial Crime

Money launderers, sanctions evaders, and terrorist financiers thrive on incomplete data. Legacy messages leave gaps that bad actors exploit.

ISO 20022 requires richer originator and beneficiary information:

- Full legal names, not truncated.

- Complete addresses.

- Purpose of payment codes (e.g., “salary,” “trade invoice,” “family support”).

- Ultimate beneficial ownership where required.

- Benefit: Transaction monitoring systems receive more context, reducing false positives and improving true positive detection rates.

- Keyword highlight: Enhanced data in ISO 20022 supports real-time sanctions screening and automated AML compliance.

3.4 For Consumers: Faster and More Transparent Payments

While end consumers rarely see ISO 20022 directly, they feel its effects:

- Faster refunds: Rich data means fewer manual reviews, so refunds process instantly.

- Clearer bank statements: Instead of cryptic codes, payments show “Invoice #1234 to Acme Corp.”

- Better fraud protection: Banks with richer data can spot suspicious patterns earlier.

- Cross-border speed: ISO 20022 enables end-to-end tracking, so sending money internationally feels more like sending a message.

- Keyword highlight: Consumer benefits of ISO 20022 include transparency, speed, and reduced friction.

Part 4: Challenges in the ISO 20022 Transition

No global standard migration is seamless. ISO 20022 adoption faces real hurdles that institutions must navigate.

4.1 Co-Existence and Translation Overhead

During the transition period, many systems must support both legacy MT and new MX messages. This means translation—converting rich ISO 20022 data down to limited MT fields or vice versa.

- The problem: Translation loses data. A 900-character remittance field becomes a 140-character truncation. Structured invoice details collapse into a single blob.

- The solution: The end goal is native ISO 20022 end-to-end, with no translation. But that will take years to achieve across all counterparties.

4.2 Implementation Costs for Smaller Institutions

Large global banks have teams dedicated to ISO 20022 adoption. Smaller banks, credit unions, and corporate treasuries may lack resources.

- Cost areas: Core system upgrades, API development, staff training, and testing with counterparties.

- Mitigation: Many BaaS and core banking vendors now offer ISO 20022-compliant modules as part of their platforms, lowering the barrier for smaller players.

4.3 Data Privacy and Cross-Border Rules

Richer data means more personal and commercial information crossing borders. This raises questions about data localization, privacy regulations (e.g., GDPR, CPRA), and information sharing between banks.

- Current approach: ISO 20022 includes optional fields for “regulatory reporting,” but banks must be careful not to send data that violates local laws.

- Keyword highlight: Compliant data sharing under ISO 20022 requires collaboration between legal, compliance, and technology teams.

Part 5: Preparing for ISO 20022 – A Guide for the Current Generation

Whether you are a fintech founder, a corporate treasurer, or a banking technology leader, specific actions will position you for success.

5.1 Audit Your Inbound and Outbound Payment Flows

Identify every payment channel that touches SWIFT, CHIPS, FedNow, TARGET, or other migrating systems. Map whether you are receiving or sending legacy MT or ISO 20022 MX messages.

5.2 Upgrade Core Systems and APIs

Legacy core banking platforms may not support ISO 20022 natively. Evaluate whether your provider offers:

- Native XML/JSON message construction and parsing.

- Schema validation tools.

- Test environments with major counterparties.

5.3 Train Teams on Structured Data

Operations, compliance, and finance teams need to understand how ISO 20022 changes their workflows. For example:

- Reconciliation now uses structured invoice fields, not free-text matching.

- Sanctions screening benefits from richer originator data.

- Exceptions handling requires new dashboards for electronic data interchange messages.

5.4 Participate in Industry Testing

Most major payment systems offer ISO 20022 test environments. Join them. Test with your banking partners before the mandatory cutover dates. Unexpected edge cases (e.g., special characters, very long fields, non-Latin scripts) are easier to fix in testing than in production.

5.5 Communicate with Counterparties

If you send payments to smaller banks or corporates that are not yet ISO 20022-ready, you may need to downgrade your messages. Agree on fallback formats and timelines with each counterparty.

Keyword highlight: Implementation readiness for ISO 20022 is a collaborative effort, not a solo technical project.

Part 6: The Future Beyond Adoption

ISO 20022 adoption is not the final destination. It is a platform for future innovation.

6.1 ISO 20022 and Artificial Intelligence

Rich, structured data is ideal for machine learning models. Banks will use ISO 20022 transaction data to:

- Predict customer cash flow needs.

- Detect fraud patterns across multiple fields.

- Offer real-time lending decisions based on invoice data.

6.2 ISO 20022 for Environmental, Social, and Governance (ESG) Tracking

Future extensions of ISO 20022 will include ESG markers—indicating whether a payment is for green energy, fair trade goods, or social impact projects. This will enable:

- Automated ESG reporting for corporates.

- Preference-based payment routing (e.g., “use a bank with high ESG scores”).

- Green bond proceeds tracking.

6.3 Convergence with Digital Identity and Verifiable Credentials

ISO 20022 messages could eventually carry verifiable credentials (decentralized identity proofs). A payment would include not just a name but a cryptographically signed attestation that the sender is a verified business. This would revolutionize know-your-customer (KYC) onboarding.

6.4 ISO 20022 as a Foundation for CBDCs

Central Bank Digital Currencies (CBDCs) need a messaging standard. ISO 20022 is the logical choice, already adopted by major central banks for high-value systems. A CBDC built on ISO 20022 would be instantly interoperable with existing payment infrastructures.

Keyword highlight: The future of financial messaging is ISO 20022-native, AI-enhanced, and increasingly automated.

Conclusion: A New Language for Global Finance

The transition to ISO 20022 is one of the most significant infrastructure upgrades in the history of finance. It replaces fragmented, limited, and aging standards with a rich, extensible, and modern language for electronic data interchange.

For the current generation of financial institutions, fintechs, developers, and corporate teams, ISO 20022 adoption is not a compliance checkbox. It is an opportunity to build faster reconciliation, smarter compliance, better customer experiences, and entirely new products that were impossible under legacy standards.

The question is no longer whether to adopt ISO 20022. The question is how quickly you can turn its rich data into a competitive advantage.

Keywords: ISO 20022 adoption, electronic data interchange, SWIFT MT vs MX, structured remittance data, real-time payments ISO 20022, FedNow messaging standard, enhanced data for AML, compliance-native standards, developer-friendly financial APIs, ISO 20022 implementation readiness, future of financial messaging, ESG in payments, CBDC messaging standard.