Banking-as-a-Service (BaaS) 3.0: The Next Generation of Platforms for Launching Compliant Financial Products in Weeks

Not long ago, building a financial product meant years of regulatory filings, millions in compliance costs, and direct relationships with legacy core banking providers. That era ended with the first wave of Banking-as-a-Service (BaaS) . Then came a second wave of middleware providers and sponsor bank arrangements. Now, a profound new shift is underway: BaaS 3.0.

Banking-as-a-Service (BaaS) 3.0 represents the next generation of platforms that allow non-banks—think e-commerce brands, gig marketplaces, B2B SaaS companies, and even influencers—to launch fully compliant financial products in weeks, not years. These products include embedded wallets, debit cards, lending solutions, rewards-as-liabilities, and savings accounts—all under the non-bank’s own brand.

For the current generation of founders, product managers, and digital-native businesses, BaaS 3.0 is not a technical back-office detail. It is a competitive necessity. Customers expect financial services to be integrated into the apps and platforms they already love. BaaS 3.0 makes that integration fast, safe, and scalable.

Below, we break down what BaaS 3.0 is, how it differs from previous generations, why it matters for today’s audience, and what real-world applications look like right now.

Part 1: The Evolution of Banking-as-a-Service – From 1.0 to 3.0

To understand BaaS 3.0, it helps to see the arc of innovation that came before.

1.1 BaaS 1.0: The API-Connected Bank

The first generation of Banking-as-a-Service was simple but limited. A fintech startup would sign a direct agreement with a chartered bank. That bank would provide a set of APIs for account opening, card issuing, and transaction processing.

- What worked: It was revolutionary for its time. Companies like Stripe, Marqeta, and Synapse (early movers) proved that non-banks could offer bank-like features.

- What failed: Each integration was custom, slow, and expensive. Compliance was still largely manual. Launch times ranged from 12 to 24 months.

- Keyword highlight: BaaS 1.0 was API-first but not compliance-native.

1.2 BaaS 2.0: Middleware and Sponsor Bank Aggregators

The second generation introduced middleware platforms (e.g., Unit, Treasury Prime, Synctera) that sat between non-banks and multiple sponsor banks. These platforms offered unified APIs, pre-built compliance workflows, and bank-partner management.

- What improved: Launch times dropped to 4–8 months. A single integration gave access to multiple banks. KYC/KYB (Know Your Customer / Know Your Business) became partly automated.

- What remained broken: Still too slow for modern product velocity. Compliance was reactive, not proactive. Many platforms struggled with bank partner risk and sudden de-risking events.

- Keyword highlight: BaaS 2.0 brought sponsor bank aggregation but still operated in a fragmented regulatory environment.

1.3 BaaS 3.0: The Compliance-Native, Real-Time, Vertical-Specific Generation

BaaS 3.0 is fundamentally different. It is not just an API layer. It is a full-stack financial infrastructure platform purpose-built for speed, safety, and specialization.

- Defining characteristics:

- Compliance-by-design: AML (Anti-Money Laundering), sanctions screening, transaction monitoring, and identity verification are embedded into every API call.

- Real-time ledgering: Every balance, hold, and settlement updates in milliseconds.

- Vertical-specific toolkits: Pre-built modules for marketplaces (escrow), gig platforms (instant payouts), or e-commerce (BNPL at checkout).

- Launch in weeks: Non-banks go from signed contract to live production in 4–8 weeks, sometimes faster.

- Keyword highlight: BaaS 3.0 is defined by compliance-native architecture and vertical-specific embedded finance.

Why the current generation cares: A product manager at a fast-growing marketplace cannot wait eight months for a card program. They need a BaaS 3.0 platform that provides a sandbox today, compliance workflows that update automatically, and the ability to pivot without renegotiating bank contracts.

Part 2: Core Components of BaaS 3.0 Platforms

What actually makes BaaS 3.0 different under the hood? Five core components.

2.1 Compliance as Code

In BaaS 3.0, regulatory compliance is not a separate review step. It is code.

- How it works: Every transaction, account opening, or payment instruction passes through automated rules that check against global sanctions lists, monitor for suspicious patterns, and enforce transaction limits.

- Examples of embedded rules:

- A new user from a high-risk jurisdiction triggers enhanced due diligence before they can receive a card.

- A sudden spike in peer-to-peer transfers flags a manual review.

- Business verification (KYB) pulls from commercial registries in real time.

- Keyword highlight: Compliance-as-code reduces manual review costs by 80% and accelerates onboarding from days to minutes.

2.2 Real-Time Ledger and Balance Management

Old BaaS systems relied on batch processing and end-of-day settlement. BaaS 3.0 operates on a real-time ledger.

- What it enables:

- A user sees their updated balance instantly after a purchase.

- A marketplace holds funds in escrow and releases them the moment a driver completes a delivery.

- A lending platform adjusts available credit in milliseconds after a repayment.

- Keyword highlight: Real-time ledgering is the difference between “pending” and “settled” disappearing from user experience.

2.3 Vertical-Specific Financial Products

General-purpose APIs are not enough. BaaS 3.0 platforms offer pre-built modules for specific business models.

- For e-commerce: Embedded BNPL, loyalty rewards as stored value, instant refunds to a branded wallet.

- For gig platforms: Instant payout cards, earnings advances based on completed trips, integrated mileage tracking.

- For B2B SaaS: Embedded invoicing with net terms, virtual cards for software procurement, revenue-based financing.

- For neobanks and challenger brands: Full checking accounts, savings pods, debit card programs with custom rewards.

- Keyword highlight: Vertical-specific BaaS allows non-banks to launch complex products without building from scratch.

2.4 Multi-Bank Orchestration with Failover

One of the painful lessons of BaaS 2.0 was sponsor bank risk. If a single bank partner changed its risk appetite or compliance requirements, entire programs could be paused.

- BaaS 3.0 solution: Platforms automatically route transactions and accounts across multiple partner banks. If one bank experiences an outage or compliance hold, traffic shifts seamlessly.

- Benefit for non-banks: No single point of failure. No sudden “program terminated” emails.

- Keyword highlight: Multi-bank orchestration provides resilience and redundancy, a non-negotiable feature for production-grade embedded finance.

2.5 Programmable Card and Wallet Infrastructure

The debit card is not a static piece of plastic in BaaS 3.0. It is a programmable object.

- What programmability means:

- A card that only works at certain merchant categories (e.g., corporate cards limited to office supply stores).

- Spend controls that reset daily, weekly, or per transaction.

- Real-time authorization decisions based on ledger balance, fraud scores, or even external data (e.g., weather for a delivery bonus).

- Keyword highlight: Programmable cards and embedded wallets turn every transaction into a logic gate.

Part 3: Why BaaS 3.0 Matters for the Current Generation

The audience of today—founders, developers, product leaders, and even end consumers—has fundamentally different expectations from those of five years ago.

3.1 Speed to Market Is Everything

A consumer brand that waits eight months to launch a loyalty card or a BNPL option will lose to a competitor that uses BaaS 3.0 and launches in six weeks. Speed is no longer a differentiator; it is a ticket to play.

- Real-world example: A direct-to-consumer (DTC) fitness brand wants to offer a branded debit card that gives 5% back on workout gear. With BaaS 3.0, they sign up, integrate the SDK, and go live in under 45 days.

3.2 No One Wants to Become a Bank

Earlier waves of fintech enthusiasm convinced some non-banks that they should pursue a bank charter. That path is expensive, slow, and distracting. BaaS 3.0 allows companies to offer financial products without becoming regulated entities themselves.

- Keyword highlight: Banking-as-a-Service means you keep your core competency (e.g., selling shoes, moving people, managing projects) while renting financial infrastructure.

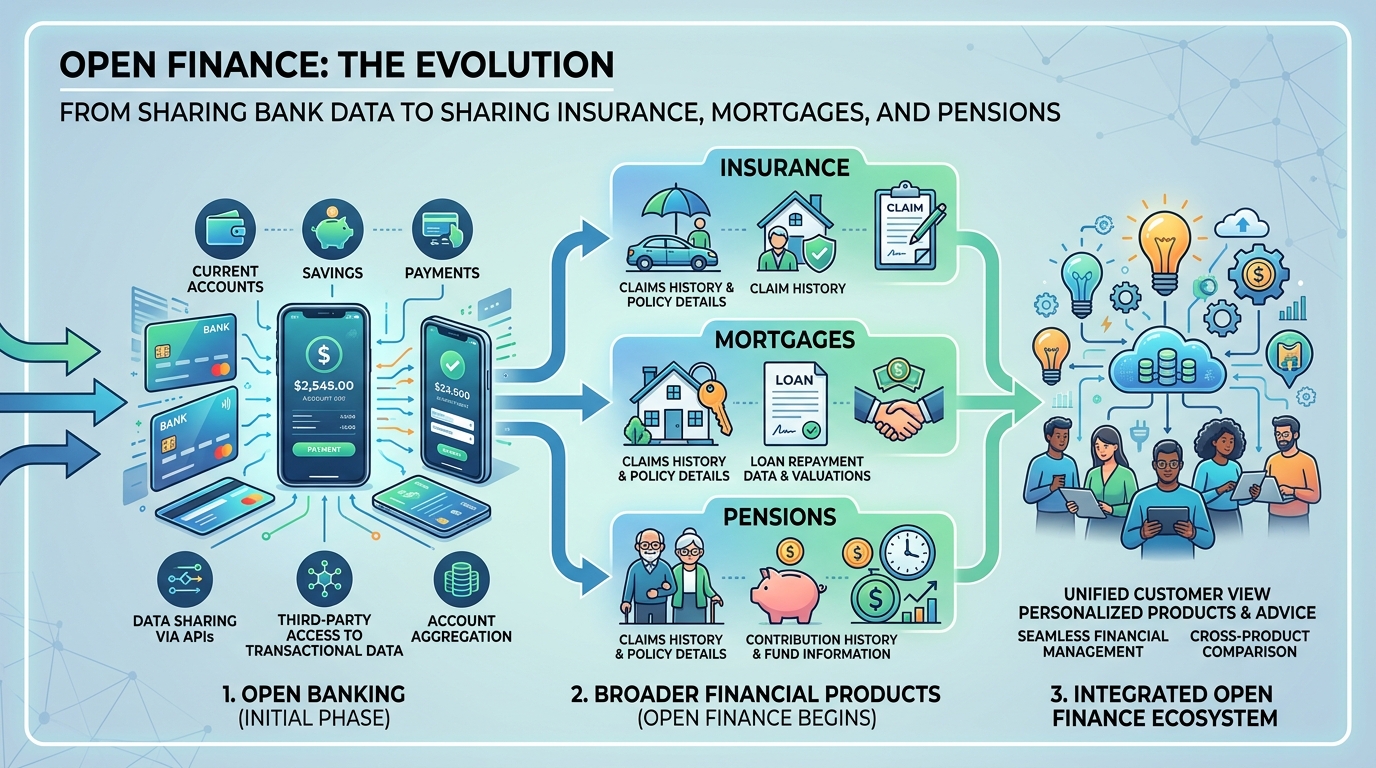

3.3 Embedded Finance Is the Expectation

The current generation of consumers does not distinguish between “app” and “bank.” They expect to store value, send money, borrow, and insure inside the apps they use daily. BaaS 3.0 makes that expectation achievable for any digital business.

- Statistic (contextual): A majority of consumers under 40 say they would switch to a non-bank brand that offers better integrated financial features. BaaS 3.0 is the engine behind that switch.

3.4 Regulatory Agility, Not Rigidity

Regulations change. New sanctions lists are published. AML rules update. BaaS 3.0 platforms bake in continuous compliance updates, so non-banks are never out of date.

- Benefit: A non-bank does not need a full-time compliance officer for basic embedded finance products. The BaaS 3.0 provider handles the regulatory heavy lifting.

Part 4: Real-World Applications and Events (Live Today)

BaaS 3.0 is not a slide deck concept. It is powering thousands of live programs across industries.

4.1 E-Commerce: Embedded Wallets and Branded Cards

Online stores are no longer just selling products; they are becoming financial hubs.

- Example: A popular apparel brand offers a branded debit card that rounds up every purchase to the nearest dollar and deposits the difference into a savings wallet. The entire experience is powered by a BaaS 3.0 platform, but the customer never sees a bank logo.

4.2 Gig and Creator Economy: Instant Payouts

Platforms for drivers, delivery workers, and content creators compete on payout speed. BaaS 3.0 enables instant earnings transfers directly to a virtual or physical card.

- Example: A freelance marketplace uses BaaS 3.0 to offer an embedded wallet where funds settle immediately after a client releases a milestone. The freelancer can spend, withdraw, or hold within the same interface.

4.3 B2B SaaS: Embedded Lending and Virtual Cards

BaaS 3.0 is transforming how software platforms monetize.

- Example: An expense management SaaS for small businesses integrates revenue-based financing. When the software detects that a business is close to its credit limit, it offers a short-term loan—originated, funded, and serviced entirely through the BaaS platform. The SaaS company earns a fee without taking balance sheet risk.

4.4 Neobanks for Specific Communities

Instead of building a general-purpose bank, BaaS 3.0 allows founders to launch vertical neobanks for truckers, nurses, real estate agents, or gamers.

- Example: A neobank for real estate agents offers commission advances (lending), errors and omissions insurance (embedded insurance), and a debit card that tracks business expenses. All built on BaaS 3.0 in months, not years.

Part 5: Choosing a BaaS 3.0 Platform – What to Look For

Not every platform claiming to offer Banking-as-a-Service is at version 3.0. Here is what current-generation buyers should evaluate.

5.1 True Compliance-Native Architecture

Ask: Is compliance an add-on or baked into the API? BaaS 3.0 platforms have automated transaction monitoring, sanctions screening, and identity verification as default, not optional.

5.2 Real-Time Ledger Visibility

Ask: Can I see every balance, hold, and settlement in real time? Can my users see the same? Delayed or batch-ledger systems belong to BaaS 2.0.

5.3 Multi-Bank Redundancy

Ask: What happens if one of your sponsor banks changes its risk policy? BaaS 3.0 platforms have failover and multi-bank routing to keep programs live.

5.4 Vertical-Specific Toolkits, Not Just APIs

Ask: Do you have pre-built modules for my industry (e.g., marketplaces, SaaS, e-commerce)? A general API is fine for developers; pre-built workflows are better for product speed.

5.5 Transparent Pricing Without Hidden Fees

BaaS 3.0 platforms typically charge a combination of monthly platform fees, per-transaction fees, and revenue share. Avoid providers with opaque “program management fees” that appear after signing.

Keyword highlight: Due diligence for BaaS 3.0 should focus on compliance-native, real-time ledgering, and vertical specialization.

Part 6: The Future of Banking-as-a-Service

BaaS 3.0 is not the end of the line. Several trends are already visible.

6.1 AI-Driven Compliance and Fraud Detection

Next-generation BaaS platforms will use real-time AI models to predict regulatory risk before transactions settle. Behavioral biometrics, device fingerprinting, and graph analysis of payment networks will become standard.

6.2 Cross-Border BaaS

Today, most BaaS 3.0 platforms are country-specific. The future is a single API that launches a financial product in multiple jurisdictions simultaneously, with local compliance handled automatically.

6.3 BaaS for Crypto and Stablecoins

As regulated stablecoin frameworks emerge, BaaS 3.0 platforms will add on-ramps, off-ramps, and yield-bearing stablecoin accounts. Non-banks will offer crypto-backed rewards without holding digital assets themselves.

6.4 Embedded Compliance as a Competitive Moat

In BaaS 3.0, compliance is not a cost center. Platforms with superior automated AML and fraud detection will win customers because they reduce risk for the non-bank.

Conclusion: The Era of Financial Product Velocity

Banking-as-a-Service (BaaS) 3.0 is here. It replaces years of regulatory slog with weeks of integration. It transforms compliance from a bottleneck into an automated advantage. It allows any digital business—e-commerce store, gig platform, SaaS company, or creator community—to launch compliant financial products under their own brand.

For the current generation, this means financial services will no longer be the exclusive domain of legacy banks. They will be features of every great app.

The question is no longer whether to adopt BaaS 3.0. The question is how quickly you can start building.

Keywords: Banking-as-a-Service (BaaS), BaaS 3.0, embedded wallets, programmable cards, compliance-native architecture, real-time ledgering, vertical-specific BaaS, sponsor bank aggregation, multi-bank orchestration, embedded finance, compliant financial products, instant payouts, revenue-based financing, programmatic compliance, vertical neobanks.