Zero-Trust Financial Architecture: Why Continuous Verification Is the New Standard in Digital Finance

In an era where digital transactions happen in milliseconds and financial data flows across borders without pause, traditional security perimeters have become obsolete. The old model—trusting users and devices once they are inside a network—no longer holds up against sophisticated cyber threats.

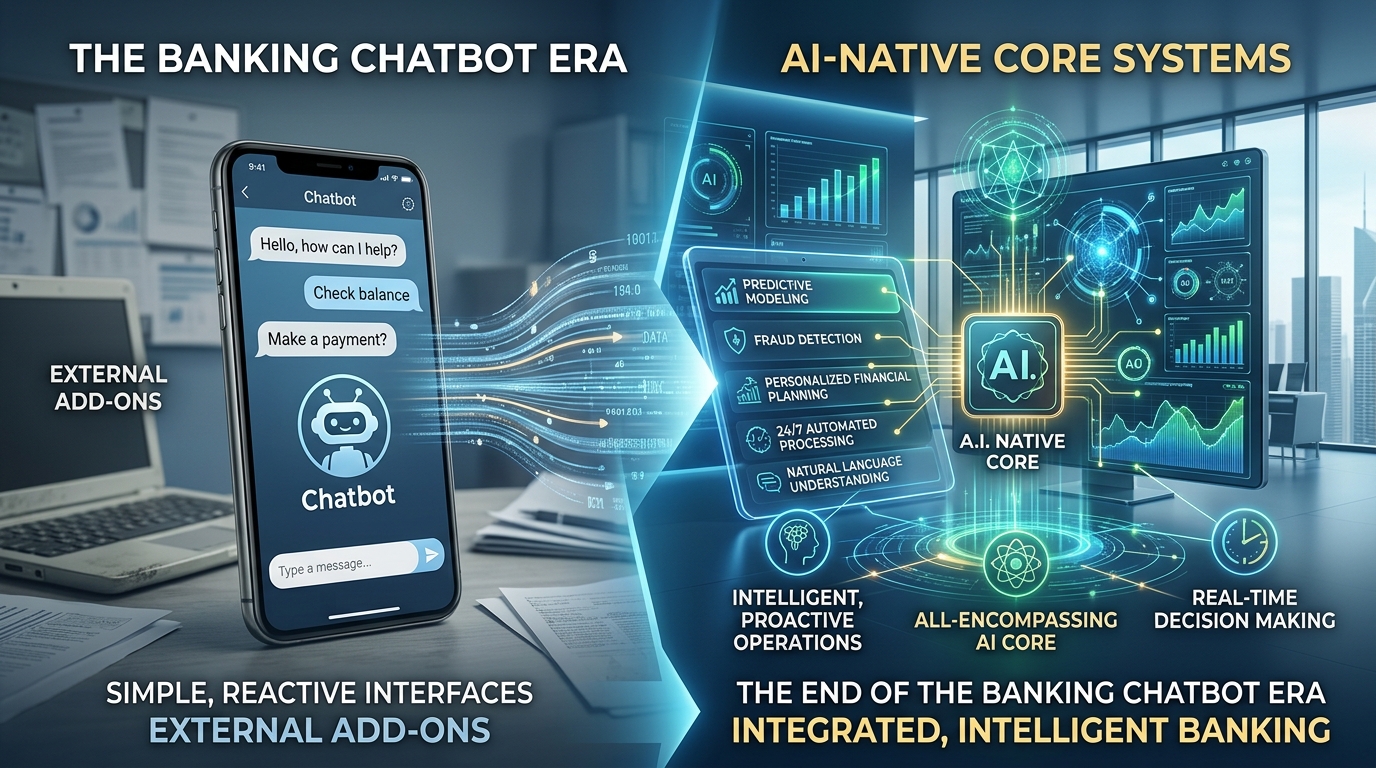

Zero-Trust Financial Architecture has emerged as the definitive security model for modern finance. It operates on a simple but powerful premise: never trust, always verify. Every user, every device, and every access request is treated as a potential threat until proven otherwise.

This article explores the core principles of zero trust in finance, why continuous verification is essential for today’s digital economy, and how financial institutions can implement this model to protect assets, data, and customer trust.

1. What Is Zero-Trust Financial Architecture?

Defining the Model

Zero-Trust Financial Architecture is a security framework designed to protect financial systems by eliminating implicit trust. Unlike legacy models that assumed everything inside a corporate network was safe, zero trust requires continuous verification for every user and every device—regardless of location.

Keyword highlight: continuous verification, every user, every device, security model, financial systems.

From Castle-and-Moat to Zero Trust

The traditional “castle-and-moat” approach relied on firewalls and VPNs to create a trusted internal zone. Once inside, users had broad access. Today, with remote work, cloud banking, and API-driven fintech, that moat has vanished. Zero trust flips the model: there is no inside vs. outside. Every request is verified in real time.

2. Why the Current Generation Needs Zero Trust in Finance

The Rise of Decentralized and Digital-First Finance

Current-generation audiences interact with money through mobile wallets, neobanks, crypto exchanges, and buy-now-pay-later apps. These platforms rely on thousands of micro-transactions and third-party integrations. Each connection is a potential attack surface.

Keyword highlight: mobile wallets, neobanks, crypto exchanges, buy-now-pay-later, attack surface.

Evolving Threat Landscape

Cybercriminals no longer just target servers. They use:

- Credential stuffing from leaked passwords

- SIM swapping to bypass SMS-based 2FA

- Man-in-the-middle attacks on public Wi-Fi

- Insider threats from compromised employee devices

Zero-trust architecture neutralizes these threats by requiring continuous verification—even after a user has logged in.

Regulatory and Consumer Pressure

Regulators like the ECB, FINMA, and CFPB now recommend zero-trust principles for payment systems. Meanwhile, customers expect real-time fraud protection without friction. Zero trust balances security and user experience using adaptive, risk-based verification.

3. Core Components of a Zero-Trust Financial System

A. Identity and Access Management (IAM)

Every user—whether a customer, employee, or contractor—must prove their identity continuously. This goes beyond passwords. Modern IAM includes:

- Biometrics (face or fingerprint)

- Hardware tokens (e.g., YubiKey)

- Behavioral analytics (typing speed, mouse movements)

Keyword highlight: Identity and Access Management, biometrics, behavioral analytics, hardware tokens.

B. Device Trust and Posture Checking

It’s not enough for a user to be who they claim. Their device must also be secure. Zero-trust systems check for:

- Outdated operating systems

- Missing security patches

- Unapproved software (e.g., keyloggers)

- Jailbroken or rooted phones

If a device fails the check, access is blocked or restricted.

C. Micro-Segmentation

Instead of a flat network, micro-segmentation divides the financial infrastructure into small, isolated zones. A payment processor cannot talk to a customer database unless explicitly allowed. This limits lateral movement in case of a breach.

Keyword highlight: micro-segmentation, lateral movement, isolated zones, breach containment.

D. Continuous Verification and Real-Time Analytics

Verification never stops. Every API call, every transaction approval, and every file access triggers a new check. Machine learning models analyze behavior patterns and assign risk scores. Anomalies—like logging in from a new country at 3 AM—trigger step-up authentication or outright denial.

4. How Continuous Verification Works in Practice

Step-by-Step User Journey

- Login attempt – User provides credentials and a push notification from an authenticator app.

- Device posture check – System scans for malware or outdated OS.

- Behavioral baseline – AI compares current behavior (e.g., swipe patterns, typing rhythm) to historical data.

- Risk scoring – Low risk = access granted. Medium risk = extra challenge (e.g., one-time code). High risk = block.

- Ongoing session monitoring – Every 5–15 minutes, or on high-value actions (e.g., transferring > $1,000), re-verification occurs.

Keyword highlight: behavioral baseline, risk scoring, session monitoring, re-verification.

Example: A User Sends a Wire Transfer

- Initial verification – Password + biometrics.

- Transaction verification – System checks if the recipient is new, if the amount exceeds usual patterns, and if the device location matches past behavior.

- Continuous check – During the session, any deviation (e.g., copying a different account number) triggers a fresh verification.

5. Benefits of Zero-Trust Financial Architecture for Current Audiences

For Financial Institutions

- Reduced breach impact – Micro-segmentation stops attackers from moving laterally.

- Compliance readiness – Aligns with PSD2, PCI DSS 4.0, and GDPR.

- Lower fraud losses – Continuous verification catches fraudulent transactions in real time.

For End Users

- Smoother experience – Adaptive verification means fewer interruptions during low-risk activities.

- Stronger privacy – Zero trust limits data exposure; even internal staff cannot see customer data without verification.

- Protection from credential theft – Stolen passwords alone are useless without device and behavioral trust.

Keyword highlight: reduced breach impact, compliance readiness, lower fraud losses, adaptive verification, credential theft protection.

6. Real-World Applications Across Finance Sectors

Retail Banking

Mobile banking apps using zero trust verify every transaction request against device ID, geolocation, and biometric signature. If a user’s fingerprint fails twice, the account is temporarily frozen.

Investment Platforms

Trading apps require continuous re-verification before executing large trades or changing beneficiary details. API access from third-party portfolio trackers is logged and throttled.

Crypto and DeFi

Decentralated finance protocols integrate zero-trust logic via smart contract-based access controls. Wallet signatures must be renewed per transaction, and suspicious activity (e.g., rapid token swaps) triggers automatic pauses.

Payment Processors

Payment gateways use zero trust to verify both merchant and customer devices during checkout. If the merchant’s POS system shows unusual API calls, the transaction is blocked.

Keyword highlight: retail banking, investment platforms, DeFi, smart contract-based access, payment gateways.

7. Implementation Roadmap for Financial Firms

Phase 1: Visibility and Asset Inventory

Before enforcing zero trust, know every user, device, service account, and API endpoint in your environment.

Phase 2: Identity Hardening

Deploy phishing-resistant MFA (FIDO2, WebAuthn). Remove SMS-based 2FA. Integrate biometrics.

Phase 3: Micro-Segmentation Rollout

Start with high-risk zones: payment gateways, customer PII databases, and trading engines. Use software-defined perimeters (SDPs) to hide resources from the public internet.

Phase 4: Continuous Monitoring and Automation

Implement security orchestration, automation, and response (SOAR) to act on risk scores instantly. For example, a detected anomaly automatically revokes session tokens and forces re-authentication.

Phase 5: User Education

Current-generation users accept zero trust when explained transparently. Show them why a second verification is needed (“Unusual login location detected”). Avoid security fatigue by minimizing friction.

Keyword highlight: phishing-resistant MFA, software-defined perimeters, SOAR, user education, security fatigue.

8. Common Myths and Misconceptions

Myth 1: Zero Trust Means No Trust

Reality: Zero trust does not distrust everyone; it verifies everyone continuously. Legitimate users pass through seamlessly.

Myth 2: It’s Only for Large Banks

Reality: Cloud-based zero-trust solutions (e.g., SASE, ZTNA) are affordable for fintech startups and credit unions.

Myth 3: Continuous Verification Slows Down Transactions

Reality: Modern systems verify in milliseconds using local biometrics and cached tokens. Users perceive no delay.

Myth 4: It Replaces All Other Security Tools

Reality: Zero trust complements firewalls, antivirus, and encryption. It adds a layer of identity-centric control.

Keyword highlight: cloud-based zero-trust, SASE, ZTNA, identity-centric control.

9. Future Trends in Zero-Trust Financial Architecture

AI-Driven Predictive Verification

Instead of reacting to anomalies, future zero-trust systems will predict risky actions before they happen—using deep learning on transaction histories and user behavior.

Passwordless Continuous Trust

Passkeys (WebAuthn) and device-bound credentials will eliminate passwords entirely. Trust is tied to the physical device and biometrics, re-verified with every interaction.

Zero Trust for Cross-Border Payments

International wire systems and central bank digital currencies (CBDCs) will adopt zero trust for interbank communication, verifying every message and settlement request in real time.

Integration with Decentralized Identity (DID)

Users will control their own verifiable credentials (e.g., “over 18” or “verified account holder”) without sharing raw data. Zero trust verifies the credential without ever seeing the underlying information.

Keyword highlight: predictive verification, passkeys, cross-border payments, decentralized identity, verifiable credentials.

10. Conclusion: The New Baseline for Financial Security

The current generation of financial services—instant, mobile, global, and increasingly decentralized—cannot rely on perimeter-based security. Zero-Trust Financial Architecture represents a fundamental shift: from static, location-based trust to dynamic, behavior-based verification.

By requiring continuous verification for every user and every device, zero trust protects against credential theft, insider threats, compromised devices, and advanced persistent threats. It satisfies regulatory demands, reduces fraud losses, and—when implemented correctly—delivers a smoother user experience.

Financial institutions that delay zero trust adoption expose themselves and their customers to unacceptable risk. Those that embrace it will lead the next decade of secure, trustworthy digital finance.

Final keyword highlight: zero-trust financial architecture, continuous verification, every user, every device, digital finance security, behavior-based verification, fraud prevention.

Ready to move beyond the castle-and-moat? Start by auditing your current access controls and implementing phishing-resistant MFA on all customer-facing and internal financial systems. The era of continuous verification is here—and it’s non-negotiable.

https://www.youtube.com/@videotat-documentary

https://twitter.com/VideoTAT_docs

https://www.facebook.com/VideoTAT.1

https://www.pinterest.com/VideoTAT/