Autonomous Finance: The Rise of Self-Managing Money

For decades, personal finance has operated on a reactive model. You spend. You check your balance days later. You manually transfer a few dollars to savings. You set a calendar reminder to pay off credit card debt. This process is not only tedious but also fundamentally broken for a generation that expects technology to handle complexity automatically.

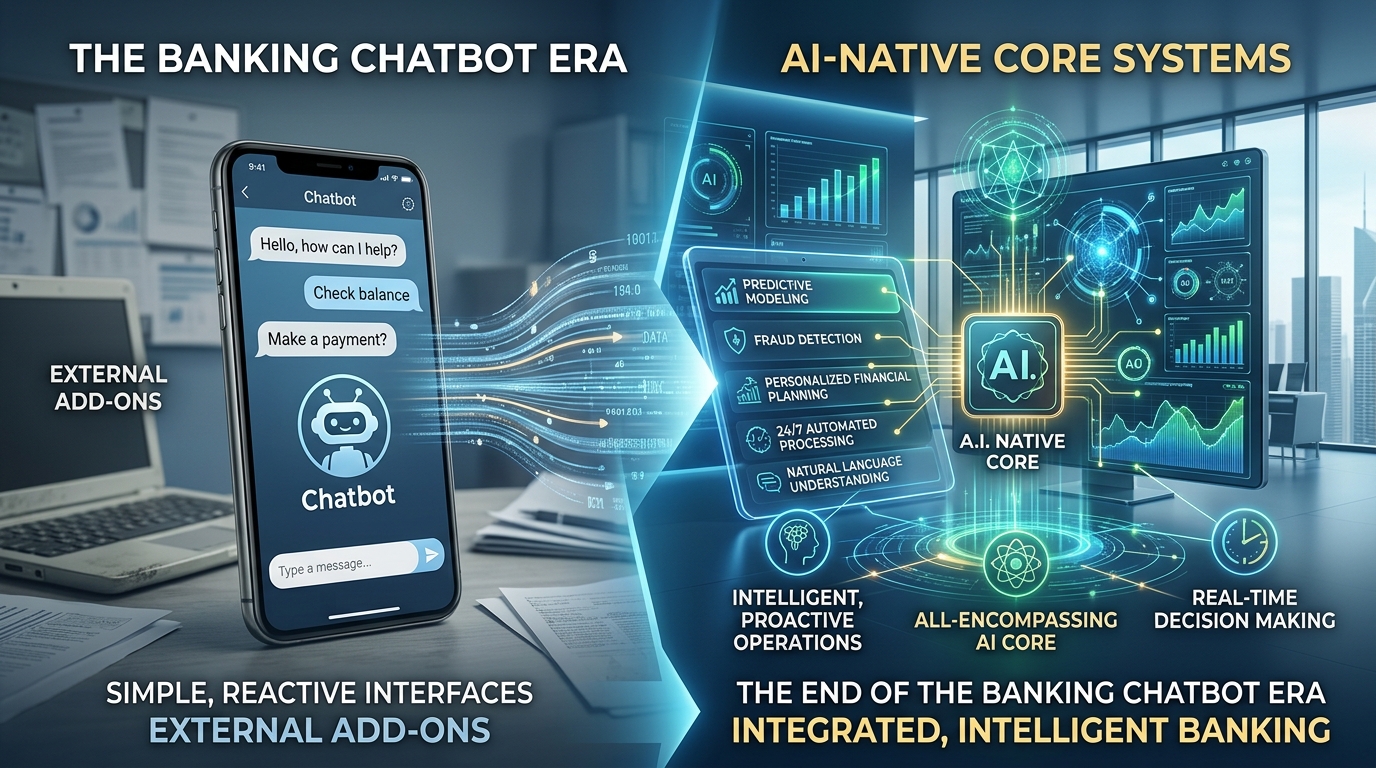

Enter Autonomous Finance—a new paradigm where financial accounts manage themselves. No spreadsheets. No monthly budgeting marathons. No guilt trips about that latte. Instead, intelligent systems continuously analyze your spending patterns and automatically move money to where it works hardest: high-yield savings accounts, debt reduction, or investment vehicles.

What Is Autonomous Finance? Moving Beyond Automated Transfers

The Difference Between Rule-Based Automation and True Autonomy

You might already use recurring transfers: “Move $50 to savings every Friday.” That is automation, not autonomy. Autonomous finance goes several steps further. It observes your real-time income, spending habits, bill due dates, and even upcoming irregular expenses. Then it makes decisions—without your manual input—to optimize your financial health.

For example, a traditional automated transfer might move $50 even when rent is due the next day, accidentally causing an overdraft. An autonomous account would pause that transfer, protect your liquidity, and reschedule the savings move for a more favorable time later in the week.

Why the Current Generation Demands Autonomous Finance

Today’s digital-native consumers have grown up with self-driving technology in everything from vacuum cleaners to vehicles. They expect their money to work the same way. The rise of gig economy income, side hustles, and irregular pay cycles has made traditional “fixed budget” methods obsolete. What works for a salaried employee with predictable monthly deposits fails completely for a freelancer whose income varies by 300% month to month.

Autonomous finance solves this mismatch by adapting to real life, not a spreadsheet fantasy.

How Self-Managing Accounts Work: The Engine Behind the Scenes

Real-Time Spending Pattern Analysis

At the core of any self-managing account is a continuous learning engine. Every transaction—your morning coffee, your utility bill, your unexpected car repair—feeds into a model that understands your unique spending patterns. The system learns:

- Which expenses are fixed (rent, insurance, loan payments)

- Which are variable but essential (groceries, gas, medical co-pays)

- Which are discretionary (dining out, streaming subscriptions, weekend trips)

More importantly, it detects behavioral shifts. If you start spending 40% more on groceries over two weeks, the system flags a potential change in circumstances—not to judge you, but to adjust its cash flow predictions accordingly.

Intelligent Surplus Detection

Legacy savings tools require you to declare an amount to save. Autonomous finance reverses the question. Instead of asking, “How much do you want to save?” it asks, “After covering all upcoming obligations, how much extra do you actually have?”

The system calculates your true surplus in real time. It considers:

- Current account balance

- Scheduled bills for the next 14 days

- Historical spending variability

- Minimum required buffers you define (e.g., “never let checking fall below $500”)

Then, it automatically moves the surplus to where it generates the most value.

Two Primary Destinations for Automated Money Movement

1. High-Yield Savings Accounts: Making Idle Cash Work

Traditional checking accounts often pay negligible interest—sometimes as low as 0.01% APY. Meanwhile, high-yield savings accounts from online banks and fintechs can offer significantly more. An autonomous system continuously sweeps idle balances into these higher-yielding vehicles.

But unlike a simple sweep account that moves everything above a threshold, autonomous finance is dynamic. If a large expense is detected on the horizon (say, annual insurance premium or holiday travel), the system holds more cash in checking temporarily. When the coast is clear, it pushes the surplus back to high-yield savings.

This means your money is never trapped. You earn higher interest without ever risking an overdraft or missing a payment.

2. Automated Debt Paydown: Smart, Not Aggressive

The second major destination for autonomously moved funds is debt reduction. But here again, nuance matters. A simple rule like “send all extra cash to the credit card with highest interest rate” can backfire if it leaves you cash-poor before a large rent payment.

Autonomous finance uses intelligent debt paydown strategies that balance interest savings against liquidity needs. The system might:

- Prioritize high-interest credit card debt during months with stable income

- Pause extra debt payments when irregular expenses spike

- Split surplus between debt and savings when both goals are urgent

Some advanced systems even optimize for credit utilization ratios, knowing that paying down a card from 80% to 30% utilization can boost your credit score faster than completely eliminating a smaller balance.

Real-World Scenarios: Autonomous Finance in Action

Scenario A: The Freelancer’s Variable Income

Maria works as a graphic designer with projects ranging from $500 to $8,000 per month. In a traditional setup, she either hoards cash (missing out on interest) or risks overspending during dry spells. With an autonomous account:

- The system detects a $7,000 client payment.

- It checks upcoming known expenses: $2,200 rent, $400 utilities, $300 estimated taxes.

- It calculates a surplus of $4,100.

- $2,000 moves to a high-yield savings account (earning interest but accessible within one day).

- $2,100 applies to her 18% APR credit card debt.

- Two weeks later, when a slow period hits, the system automatically reverses $500 from savings back to checking to cover groceries—no overdraft, no stress.

Scenario B: The Two-Income Household with Sporadic Debt

James and Taylor both work salaried jobs but carry multiple debts: a car loan at 5%, student loans at 4%, and a store card at 22%. Their autonomous system learns their joint spending patterns: high restaurant spending in summer, higher utility bills in winter, and an annual vacation withdrawal every August.

The system’s algorithm determines that aggressive debt paydown is possible from September through November and again from February through April. During summer months, it shifts to a balanced mode, moving smaller surpluses to high-yield savings to fund vacation spending without debt. Over 12 months, they pay off the store card entirely and reduce the car loan principal by 40%—all without manually adjusting a single transfer.

The Technology Stack: How Autonomous Finance Stays Safe and Smart

Continuous Learning Without Manual Rules

Unlike old-school “if this, then that” automations, autonomous finance relies on predictive models that update daily. These models are trained on anonymized transaction data to recognize patterns like:

- “Users in this income bracket typically see a 30% spending increase in December.”

- “After three consecutive months of debt paydown, the risk of cash flow shock rises by 15%.”

The system does not follow your commands; it follows your revealed preferences—what you actually do, not what you say you will do.

Security, Control, and Human Oversight

A common concern with autonomous finance is loss of control. Responsible implementations address this through:

- Hard and soft guardrails: You set absolute boundaries (e.g., “never move more than $2,000 in a single day”) alongside adaptive parameters (e.g., “prioritize debt paydown unless checking drops below $1,000”).

- Real-time notifications: Every automatic move is logged and explained in plain English, often with a one-click reversal option for two to 24 hours.

- Scenario previews: Before enabling full autonomy, you can run a simulation showing how the system would have handled the past three months of your actual transactions.

Why Autonomous Finance Is Not Just for High Earners

A persistent myth is that automated money movement only benefits people with large surpluses. The opposite is true. Autonomous finance provides the most dramatic improvement for those with tight or variable cash flow.

A high earner with $10,000 monthly surplus might not notice if $200 sits idle. But a gig worker who can only save $50 some months and nothing in others needs every dollar optimized. By automatically detecting small windows of surplus—$15 here, $40 there—autonomous accounts aggregate “micro-savings” that would otherwise leak unnoticed.

The Competitive Landscape: Banks vs. Fintechs vs. Neobanks

Incumbent Banks Playing Catch-Up

Traditional banks have been slow to offer true autonomous features. Most still push “round-up” apps (save your spare change) as innovation. While useful, round-ups are a pale shadow of full self-managing accounts. A round-up saves pennies; autonomous finance moves hundreds or thousands of dollars intelligently.

Fintech and Neobank Leadership

Younger financial institutions—often digital-only—are leading the autonomous charge. They build from the ground up with event-driven architectures, real-time ML inference, and user interfaces designed for transparency. Features like automated debt paydown and dynamic savings sweeps are becoming flagship offerings, attracting customers tired of manual budgeting.

Getting Started with Autonomous Finance Today

Step 1: Audit Your Current Automation

Review any recurring transfers or savings rules you have set up. Are they still appropriate for your current income and spending? Most people set rules once and never revisit them. Autonomous systems, by contrast, adjust continuously.

Step 2: Look for Core Features in a Financial App

When evaluating a bank or fintech app, search for these keywords: spending pattern analysis, automated surplus detection, high-yield savings integration, and dynamic debt paydown. If a product only offers fixed recurring transfers or round-ups, it is not truly autonomous.

Step 3: Start with Guardrails

Enable autonomous features with conservative limits—for example, “move surplus above $2,000 only” or “pay down debt but never reduce checking below two months of expenses.” As you build trust in the system, you can expand its authority.

Conclusion: The End of Manual Money Management

Autonomous finance represents a fundamental shift in how humans interact with their money. The old way—tracking every expense, manually moving funds, worrying about timing—belongs to a past era of scarcity and friction. The new way is self-managing accounts that observe, predict, and act on your behalf.

By automatically moving idle cash to high-yield savings accounts and intelligently accelerating debt paydown based on your real spending patterns, these systems deliver better financial outcomes with less effort. The current generation, raised on seamless digital experiences, will not settle for anything less.

Your money should work as hard as you do. And with autonomous finance, it will finally be—without you having to lift a finger.